{kind=link}

It’s been greater than two years since I wrote an evaluation primarily based on Surplus Line Affiliation of California perception and knowledge for an Insurance coverage Journal article forecasting that the state’s owners insurance coverage market was coming into a structural transition pushed primarily by inhabitants decline, inflation and admitted‑provider exits.

On the time, new extra and surplus coverage depend was solely starting to rebound after a number of years of contraction, and the information instructed that broad socioeconomic forces—somewhat than disaster tendencies—had been setting the stage for change.

Associated: ‘Structural Shift’ Occurring in California Surplus Traces

In a March 2025 Insurance coverage Journal evaluationI used SLACAL knowledge to doc how the traits of newly written surplus strains houses had shifted dramatically. Decrease‑worth, decrease‑danger, historically admitted‑market houses had been coming into surplus strains in giant numbers. Alternative prices, assessed values, sq. footage and burn chance all fell sharply, with premiums following the identical downward trajectory. These modifications painted a transparent image: The surge was being pushed not by heightened danger, however by displacement.

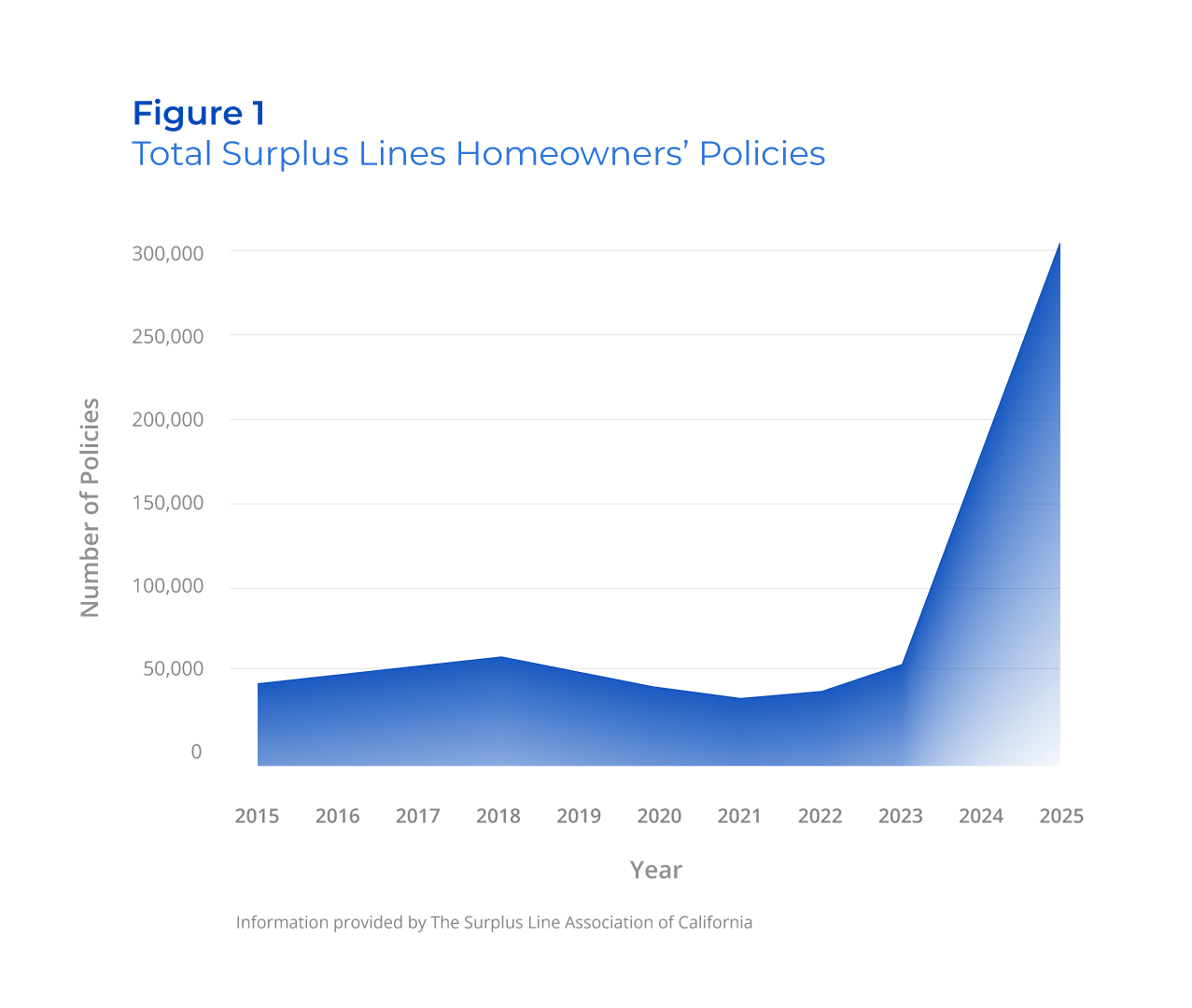

Immediately, with one other full yr of information, the pattern has superior into a brand new—and much more surprising—part. As proven in Determine 1, whole surplus strains owners insurance coverage insurance policies didn’t merely proceed rising—they spiked previous 300,000 in 2025, a degree with out precedent. What had been a rebound in 2023, and a structural shift in 2024, has now develop into a full‑scale realignment of the place California owners acquire protection.

Wildfire Danger Nonetheless Falling, At the same time as E&S Owners Rely Climbs

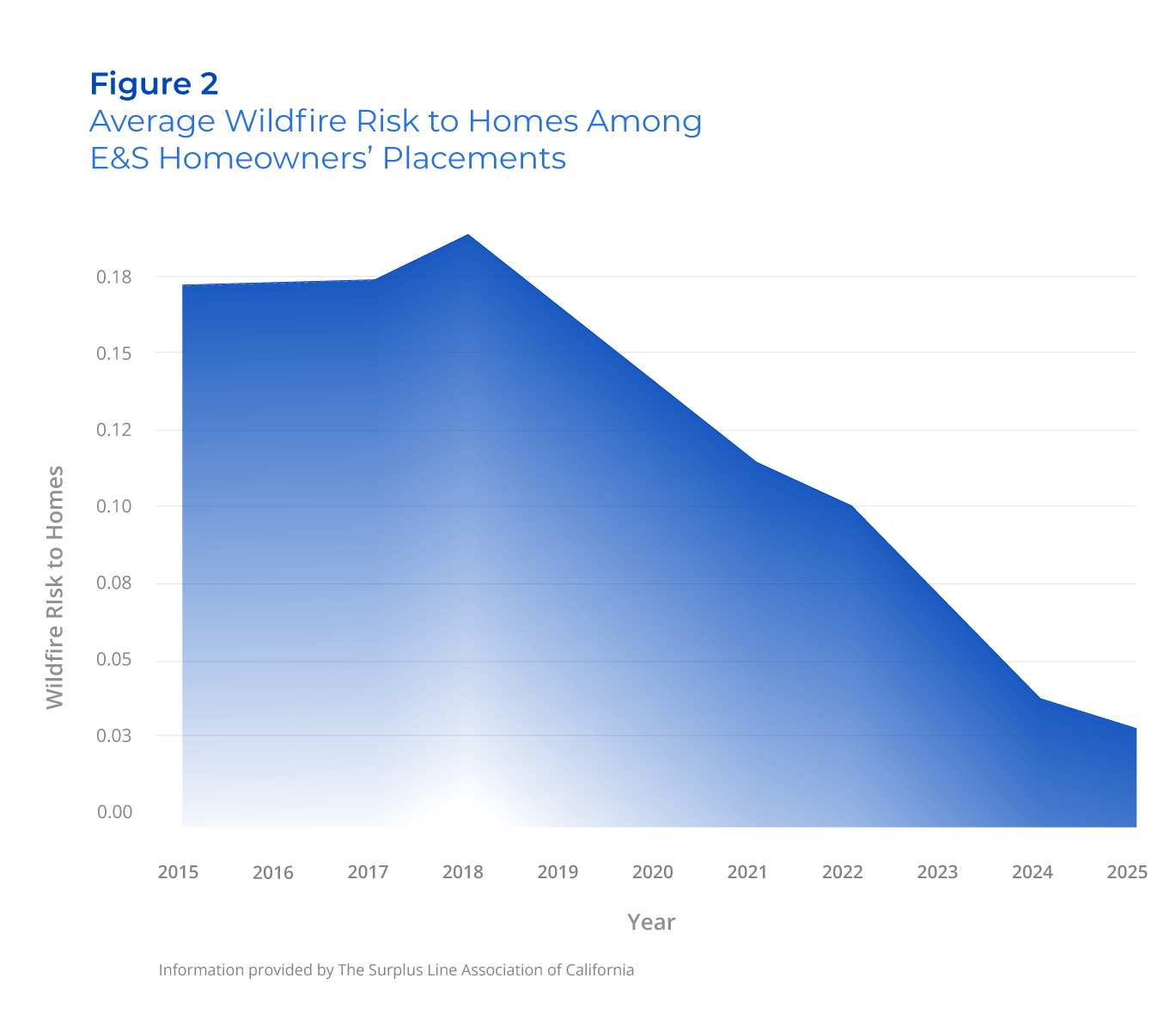

My earlier 2025 evaluation used burn chance as the first hazard metric. Right here, I exploit wildfire metrics from the U.S. Division of Agriculture Forest Service’s 2024 Wildfire Danger to Communities dataset, together with danger to houses and publicity sort.

Danger to houses combines the chance of wildfire, modeled fireplace depth and potential construction injury, offering a extra property-specific view of hazard. When SLACAL first reported the decline in wildfire hazard in 2025, it seemed to be a brief artifact of admitted‑market stress. As a substitute, the pattern has strengthened. As proven in Determine 2, portfolio‑extensive danger to houses has now fallen to its lowest degree, persevering with a multi-year decline whilst E&S quantity surged previous 300,000 insurance policies. This sample continued regardless of California’s extreme 2025 wildfire season and the ensuing pressure on insurer capital. Whereas admitted carriers understandably restricted new enterprise, the houses coming into E&S in 2024 to 2025 confirmed decrease, not increased, underlying wildfire hazard.

The message is obvious: The surge in surplus strains exercise will not be being pushed by worsening hazard, however by protection shortage, echoing the structural forces highlighted within the introduction.

A Stunning Pivot: E&S Has Turn into City

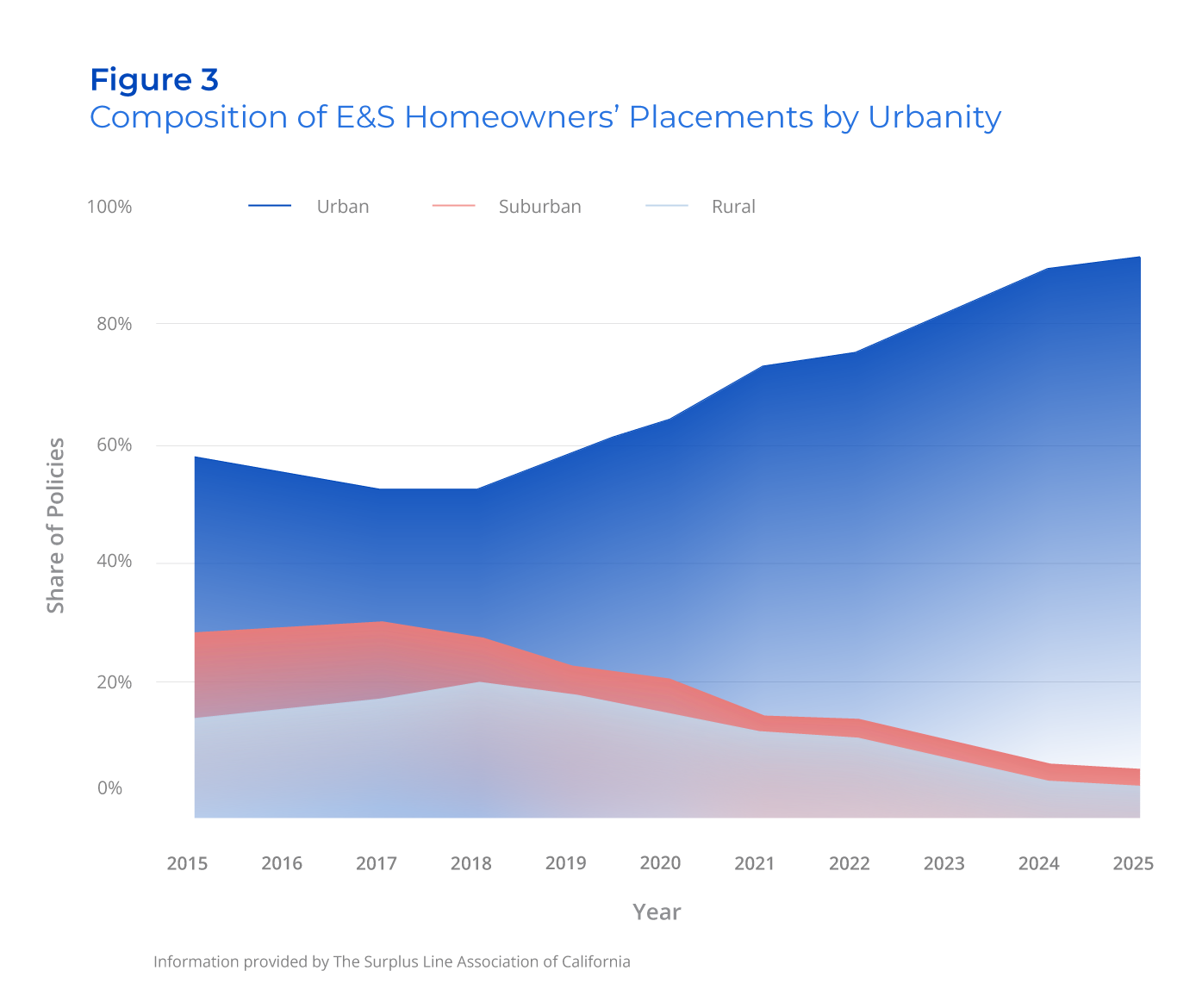

Maybe essentially the most putting growth is the place the brand new surplus strains enterprise is coming from. Traditionally, E&S owners’ insurance coverage has been related to increased‑danger rural or Wildland-City Interface (WUI)‑adjoining properties—houses located close to wildland fuels, on the fringe of the constructed setting, or in locations the place ember publicity from close by vegetation was a significant driver of wildfire loss potential. However the latest yr of information overturns that assumption totally.

As proven in Determine 3, city houses—labeled utilizing 2020 rural–city commuting space codes from the U.S. Division of Agriculture Financial Analysis Service—represented roughly 80% of all E&S placements in 2023, elevated to almost 89% in 2024, and reached about 90% in 2025, whereas suburban and rural shares contracted into the low single digits. E&S carriers are now not primarily insuring fringe geographies or gasoline‑adjoining houses—they’re more and more writing normal metropolitan properties, the very houses that traditionally outlined the admitted market.

This shift is seen not simply in shares however in focus throughout California’s main cities. In 2025, Los Angeles (5.8%) and San Diego (5.3%) collectively accounted for roughly one-in-nine E&S owners’ placements statewide, with San Francisco (2.1%), Sacramento (1.7%), and San Jose (1.7%) rounding out the highest 5—16.6% collectively (practically 50,000 insurance policies). These concentrations underscore that the surge is centered in main metropolitan areas, not in rural or WUI‑adjoining communities.

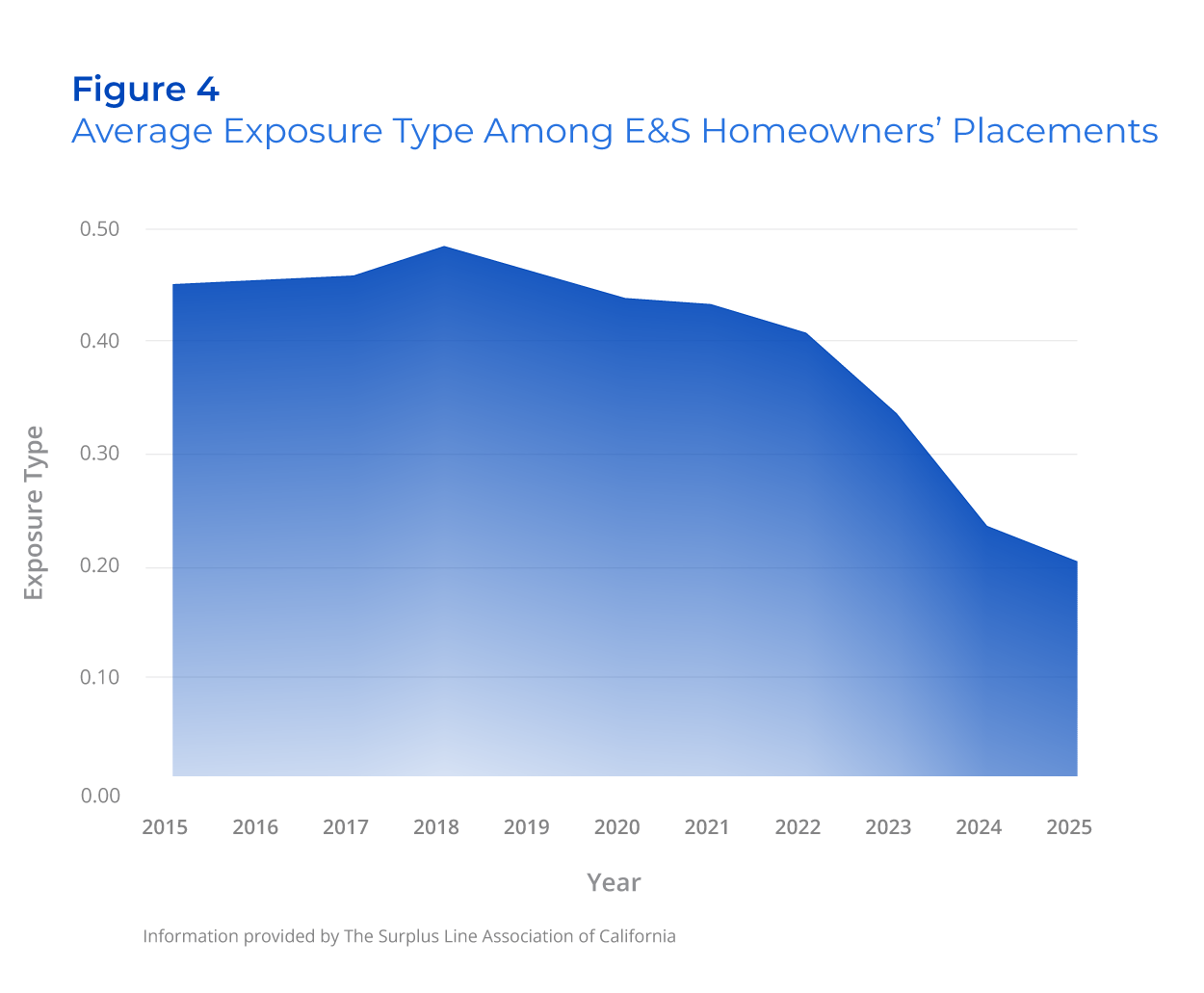

This shift is independently strengthened by the pattern in publicity sort, proven in Determine 4. On this evaluation, publicity sort represents the modeled diploma to which a location is uncovered to close by wildland fuels, with values starting from 1 (direct publicity inside burnable vegetation) to 0 (little to no modeled publicity). Portfolio‑extensive publicity sort has declined sharply, falling from 0.44 in 2020 to 0.34 in 2023, after which to 0.20 by 2025. This means that the properties coming into E&S have gotten much less related to wildland fuels.

The convergence of those two patterns—a rising city share (Determine 3) and falling publicity sort (Determine 4)—offers compelling proof that the growth of E&S owners insurance coverage will not be pushed by better hazard or elevated WUI proximity. As a substitute, it displays a structural market transition formed by protection shortage within the admitted market, not disaster‑pushed displacement. Surplus strains carriers are now not absorbing solely the outliers—the customized houses, the extremely uncovered dangers or the onerous‑to‑place rural properties. They’re more and more insuring extraordinary city houses whose danger traits look essentially just like these lengthy related to the admitted market.

Put merely, the E&S market has not develop into riskier. It has develop into extra city and fewer uncovered—a change pushed by entry constraints somewhat than hazard escalation.

A Story of Transformation

Throughout our 2024, 2025, and now 2026 analyses, a coherent narrative has emerged:

2024: Macro Forces Start the Shift

Inhabitants decline, inflation and admitted‑provider exits set off the primary main rebound in E&S new enterprise.

2025: Admitted‑Market Dangers Flood into E&S

Alternative prices, assessed values, sq. footage and wildfire hazard all fall sharply as houses historically written within the admitted market shift into surplus strains.

2026: The Shift Deepens and Expands

Wildfire danger to houses reaches historic lows amongst E&S placements, and each the rise in city participation and the sharp decline in publicity sort present that the market is now not outlined by hazard or WUI adjacency—it’s outlined by entry constraints. By 2025, practically nine-in-10 E&S houses had been in city settings, and publicity sort fell to its lowest degree, confirming that the surge displays the place customers lack admitted‑market choices.

Put otherwise: E&S has gone from area of interest → spillover → parallel market.

What This Means for the Future

As surplus strains carriers more and more insure houses that pose no better hazard than the median admitted‑market danger—and in lots of instances are each city and low in publicity sort (Figures 3 and 4)—a number of necessary implications emerge:

- The boundary between admitted and surplus strains is now blurred. For a lot of owners, E&S now features much less as a security valve and extra as the sensible different when admitted‑market choices slim.

- Market stability now is determined by regulatory modernization. Admitted carriers’ skill to return at scale will hinge on score frameworks that extra successfully align value with evolving prices and underlying danger.

- Surplus strains carriers face new portfolio dynamics. An inflow of decrease‑danger, decrease‑worth and more and more city houses reshapes underwriting assumptions, pricing expectations and lengthy‑time period capital wants.

- Customers are bearing the price of capability shortages. Protection challenges more and more replicate market construction and regulatory constraints.

Importantly, there are early indicators of a possible pivot. In late 2025, Farmers Insurance coverage eliminated its cap on new owners insurance coverage insurance policies and filed a sustainable insurance coverage technique–aligned score plan whereas making ready direct outreach to a whole lot of 1000’s of customers in distressed areas. Whether or not this marks the start of broader admitted‑market re‑entry—or just a brief easing of stress—stays to be seen.

E&S Is No Longer an Exception—It’s Changing into the Default

From the socioeconomic pressures of 2024, to the danger‑profile inversion of 2025, to the sharp declines in wildfire hazard and the city surge of 2026, California’s owners’ insurance coverage market has undergone a structural realignment. The information now present that the E&S market is now not merely responding to excessive‑danger or onerous‑to‑place properties. It’s responding to a systemic scarcity of admitted‑market capability—absorbing owners who traditionally would by no means have entered surplus strains.

Crucially, this transition is strengthened on each dimension of wildfire‑associated danger. Danger to houses is falling to file lows (Determine 2), publicity sort continues to say no (Determine 4) and the E&S e-book has develop into overwhelmingly city (Determine 3). These tendencies all level in the identical course: The houses coming into surplus strains have gotten much less hazard‑uncovered and extra metropolitan.

This can be a market entry story, and it might be the defining insurance coverage problem for California within the years forward. The predominance of city placements—mixed with traditionally low publicity sort—underscores that the market is absorbing mainstream houses somewhat than hazard‑uncovered fringe properties. E&S is now not an exception. It’s changing into the default.

Gorshunov, Ph.D., is an information scientist at The Surplus Line Affiliation of California.

Prime picture: Crews sift via bunt construction following the 2025 Eaton Hearth. Picture by CalFire.

Matters

Disaster

California

Pure Disasters

Wildfire

Extra Surplus