{kind=link}

Following the “paradigm-shifting” Los Angeles wildfires in January, the 2024-2025 wildfire season might be remembered as a turning level for the insurance coverage business, and a warning that “wildfire is now not a seasonal or rural phenomenon,” a brand new outlook asserts.

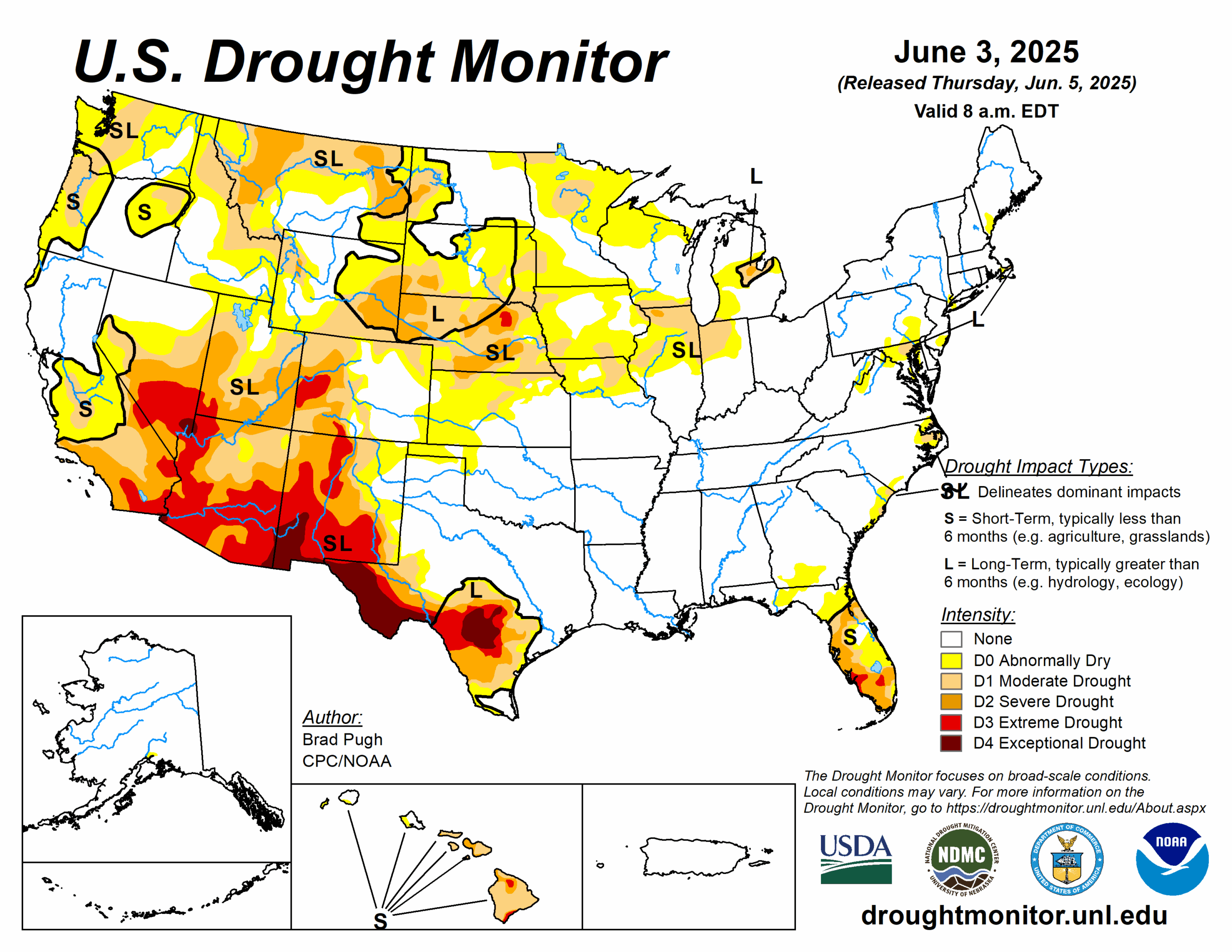

The remainder of 2025 poses extreme wildfire threat in quite a few states because of growing drought situations, together with excessive threat in wildfire-prone California, in accordance with a report from ZeztyAI.

The L.A. wildfires killed 29 folks, and broken or destroyed hundreds of properties. The fallout of the fires included giant losses for main California insurers, together with State Farm. The service is asking the California Division of Insurance coverage to approve a big price enhance. Based on the California Division of Insurance coverage, 37,749 claims have been filed associated to the fires and $12.1 billion has been paid out.

Nevertheless, the wildfire perils weren’t solely in California.

Associated: Owners Suing USAA and AAA Insurers Over LA Wildfires

“From New Mexico, the place one of many state’s most harmful wildfires validated early high-risk forecasts, to blazes within the Midwest and Southeast, the 2024 season revealed wildfire’s increasing geographic footprint, relentless tempo, and more and more unpredictable habits,” the report acknowledged. “For insurance coverage carriers, it uncovered the bounds of legacy fashions nonetheless tied to historic fireplace perimeters or broad geographic zones, and accelerated adoption of next-generation instruments that assess parcel-level vulnerability—together with structural options, defensible area, and vegetation overhang.”

The remainder of the 12 months is shaping as much as be extra unstable following a average 2024 wildfire season. Extreme drought situations are anticipated to return and unfold throughout the nation, with intensified dryness within the Southwest and deep into the Northern Rockies and the Plains, in accordance with the report.

“Heavy rains in California, Oregon, and Washington through the previous two years have pushed vital vegetation development. If warmth and dryness persist into late summer time as forecasted, these areas might as soon as once more turn out to be extremely flamable,” the report states. “This acquainted sample, the place moist years increase gasoline hundreds that flip harmful when situations shift, stays a long-term driver of wildfire threat in these traditionally weak states.”

Associated: Invoice to Deal with California Wildfire And Insurance coverage Crises Shifting By means of Legislature

The report notes that states like Arizona, New Mexico, Nevada, Utah, and Colorado stay in multi-year droughts, whereas Montana, Wyoming, North Dakota, and South Dakota are rising as new high-risk zones attributable to a dry, snow-starved winter and unusually heat spring. Drought indicators are additionally popping out of Texas and Florida, in accordance with the report.

The report additionally touches on how new state guidelines and legal guidelines are reshaping how insurers are assessing and speaking threat:

- In late 2024, the California Division of Insurance coverage finalized its Sustainable Insurance coverage Technique, a reform to stabilize the state’s insurance coverage market. Central to the technique is the approval of forward-looking disaster fashions in price filings—permitting insurers to cost wildfire threat primarily based on future publicity relatively than previous losses.

- In 2025, Colorado enacted Home Invoice 25-1182, establishing a brand new benchmark for transparency in wildfire threat modeling. The regulation applies to all admitted carriers and the FAIR Plan. It requires insurers to reveal how wildfire fashions impression charges, acknowledge each property- and community-level mitigation efforts, notify policyholders yearly of their threat scores and reductions and supply an appeals course of for disputed scores.

- In 2024, Washington adopted new rules geared toward enhancing transparency round insurance coverage premium will increase. Insurers are required to inform policyholders that they could request a written clarification for any enhance of their householders or auto insurance coverage premiums. Upon request, carriers should present a rationale inside 20 days.

- In April, Oregon handed Senate Invoice 83, repealing the state’s obligatory wildfire hazard map following sustained public opposition. The unique map had categorised properties into threat zones that triggered defensible area necessities and stricter constructing codes—measures that some property house owners argued have been primarily based on incomplete or inaccurate knowledge and had unintended penalties on insurance coverage availability and property values.

Subjects

Disaster

Pure Disasters

Wildfire

Louisiana

Involved in Disaster?

Get computerized alerts for this matter.